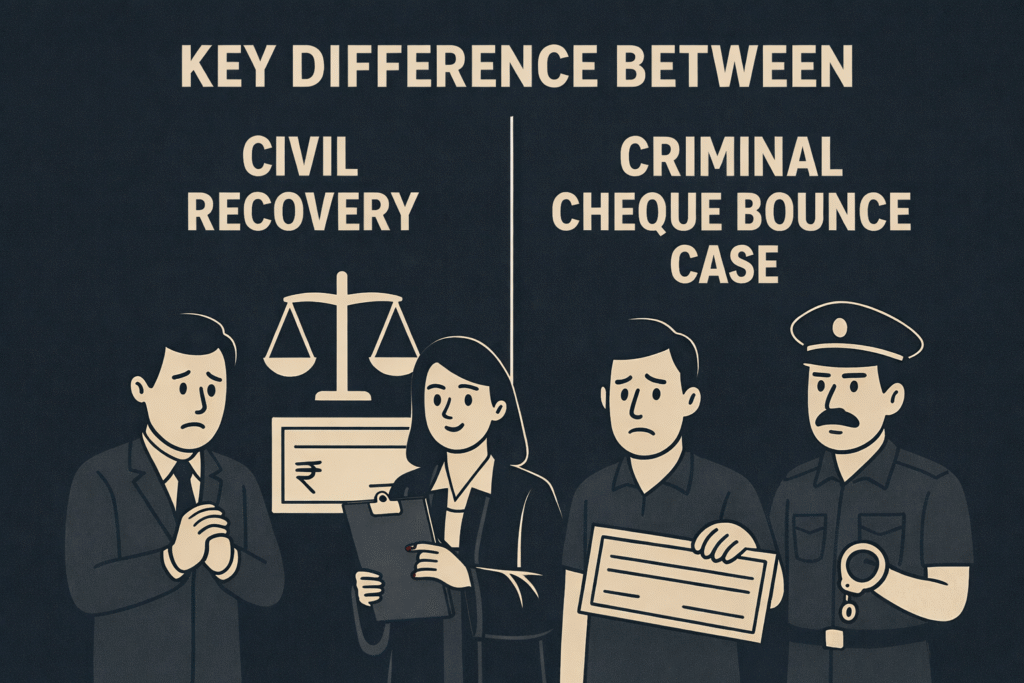

Financial disputes are a common part of modern commercial dealings, especially when loans, business credit, and cheques are used extensively. When a person fails to repay money, the aggrieved party often wonders whether to file a civil suit for recovery or pursue a criminal complaint under Section 138 of the Negotiable Instruments Act, 1881. Although both remedies aim to address monetary default, they differ fundamentally in their nature, process, and outcome. Understanding these differences helps litigants and lawyers choose the most effective strategy.

A civil recovery action is purely a civil proceeding based on breach of contract or non-payment of a legally enforceable debt. It does not matter whether the payment was expected through a cheque, cash, bank transfer, or any other mode. The plaintiff approaches the civil court seeking a decree for recovery, along with interest and damages where applicable. The court examines the case on the standard of “preponderance of probabilities,” meaning the plaintiff only needs to show that their version is more likely to be true than not. Civil suits may be filed under the Code of Civil Procedure, including as a summary suit under Order XXXVII, which is particularly suitable for cheque-based or written contract claims.

In contrast, a case under Section 138 of the NI Act is a criminal proceeding, aimed at punishing the dishonour of a cheque issued towards a legally enforceable debt. The NI Act provides a strict timeline: the cheque must be deposited within its validity, a legal notice must be issued within 30 days of dishonour, and if payment is not made within 15 days of receiving the notice, a complaint must be filed within the next 30 days. Once the complainant proves issuance and signature on the cheque, the court draws a legal presumption under Sections 118 and 139 that the cheque was issued towards a debt.

While civil recovery aims solely at compensating the creditor, Section 138 proceedings serve a dual purpose: protecting the credibility of cheque transactions and deterring defaulters. The punishment may include imprisonment up to two years or a fine up to twice the cheque amount. Notably, courts increasingly encourage settlement and compounding of Section 138 cases, as seen in Damodar S. Prabhu v. Sayed Babalal H., in which the Supreme Court laid down graded costs to facilitate compounding at different stages of the case. Section 138 NI Act case is triggered only when a cheque is dishonoured for reasons like insufficient funds or stop payment. This remedy is criminal in nature, intended to protect the credibility of cheque transactions and discourage defaults. Once the issuance and signature of the cheque are shown, the law presumes it was issued for a legally enforceable debt—shifting the burden to the accused. Punishment may include imprisonment up to two years, fine up to twice the cheque amount, and compensation. Recent judgments also encourage early compounding, making these cases efficient for negotiation and settlement.

Importantly, both remedies can run simultaneously. A civil suit secures the monetary claim, while a 138 complaint creates effective pressure and often speeds up resolution. In practice, using both together provides the strongest strategy for recovering dues.